Student Debt Repayment Guide

Illustrations by Scott Snider

The Problem:

Student debt is the great financial disruptor for anyone with a significant debt load.

Many young professionals with both student debt and a house find themselves carrying 2 mortgage-like payments. It often means sacrificing saving enough for retirement, delaying necessary upgrades to the house, or not having an adequate emergency savings. Worse yet, credit card debt can snowball and create a larger deficit.

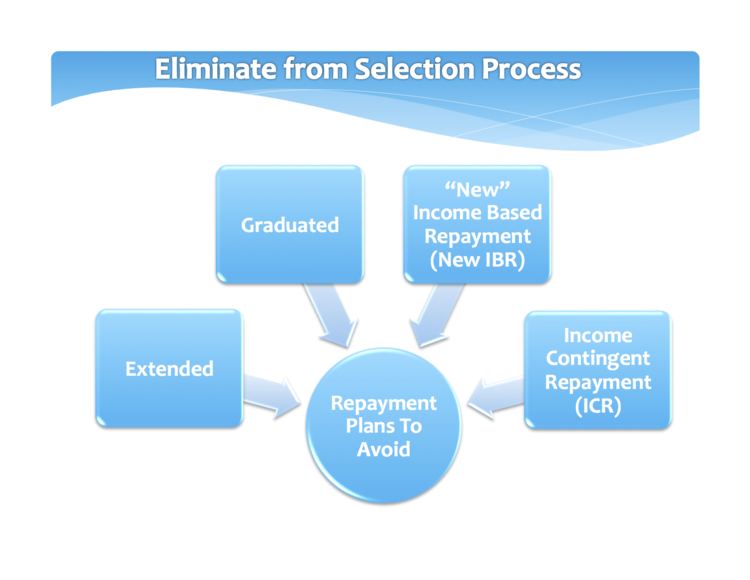

Be aware that the default plan for Federal student loans is the 10-year standard plan when no action is taken.

Avoid these plans. They are outdated or have more expensive drawbacks compared to "Old" IBR, PAYE, REPAYE, and the 10-year standard plan.

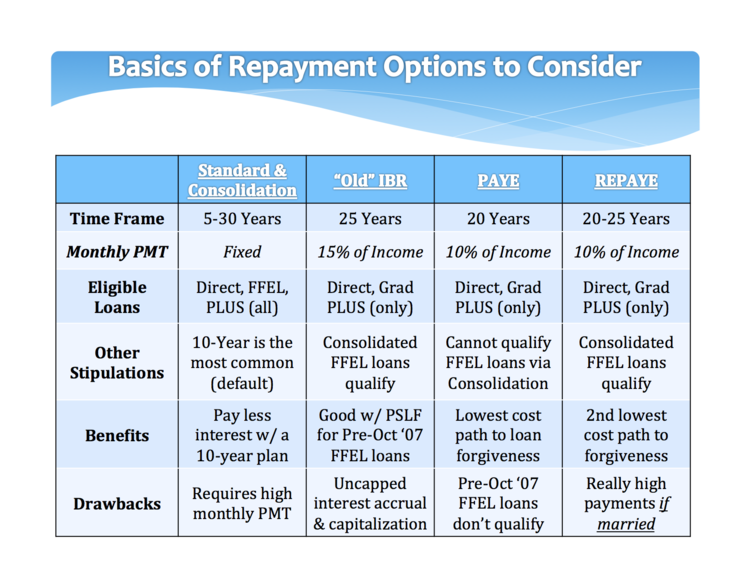

The most effective way to lower your monthly payments is through PAYE or REPAYE.

PAYE is normally the preferred choice because it offers the fastest way to debt forgiveness (20 years vs. 25 years), but REPAYE is more effective at reducing interest accrual costs. Avoid REPAYE if you are married filing taxes separately.

Avoid REPAYE if you are married filing separately on your tax returns. The spouse's income is automatically included with REPAYE, so filing separately did nothing in the way of helping you reduce your payments.

Always compare refinancing Federal debt to PAYE, REPAYE, and IBR before signing the dotted line because there's no turning back once the loans are refinanced.

A good financial plan for millennials starts at the foundation, which is solving the riddle that is student debt. After that domino falls the other pieces, like retirement and buying a house, begin to fall in place.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Paragon Wealth Strategies, LLC [“Paragon”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Paragon. Please remember that if you are a Paragon client, it remains your responsibility to advise Paragon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Paragon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Paragon’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.wealthguards.com. Please Note: Paragon does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Paragon’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Also Note: IF you are a Paragon client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.