4 Reasons Your Retirement Plan Might Fall Short

Ever find yourself daydreaming about retirement? Whether your dream retirement entails traveling the world, dedicating time to beloved hobbies, or helping your children and grandchildren, saving enough for retirement is critical to enjoying all of these endeavors. Everyone deserves the best retirement possible, but numerous planning mistakes can cause retirement plans to fall short.

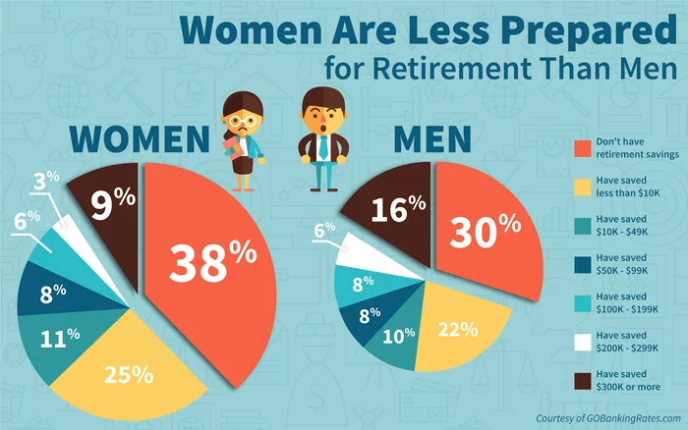

According to recent studies, retirement savings look grim for many Americans for reasons such as living longer, expensive medical care, and the rising cost of living. One survey showed that 45% of all Americans have saved nothing for their retirement, including 40% of Baby Boomers. This trend continues with younger generations too, with a recent report from The National Institute on Retirement Security showing that 66% of Millennials haven’t saved a penny towards their retirement.

If you have started saving for retirement, you’re definitely ahead of the curve. However, you could still be engaging in some of the biggest retirement planning mistakes—without even realizing it. How can you save enough to thoroughly enjoy your ‘golden years,’ without hurting your finances in the meantime? Here are 4 retirement planning mistakes worth avoiding:

Mistake #1: Focusing on the Return Rate

If you have an investment that produces a high rate of return, it’s easy to get caught up in always pursuing that outcome. However, be wary of that type of bias, as it could negatively impact your future investments. Rather than chasing rates of returns, shift your focus to creating a diversified portfolio that spreads out investments through a variety of fund types. This might include balanced, index, equity, or global. Working with a financial advisor that helps you diversify your portfolio can help protect your retirement savings if/when the economy goes sideways. Plus, they’ll help you discover investments that match your retirement goals and risk tolerance.

Mistake #2: Retiring Too Early

Many of those saving for retirement aren’t saving as much as they need to continue their lifestyle during retirement. If that sounds like your situation, then possibly consider staying in the workforce a little longer and wait to take your Social Security benefits. This will allow you to save longer and also maximize your benefits if you don’t apply for them at age 62.

Additionally, Social Security data shows that around 33% of retirees live until 92 years old, and 75% of retirees apply for benefits as soon as they hit 62. With this in mind, pushing retirement back a bit could benefit you in the long-run.

With that said, pushing back retirement isn’t the best option for everyone. There are many reasons to retire as soon as you can, such as having health issues or other life circumstances that encourage early retirement. Whether you plan to retire early or need to retire later than expected, working with a financial advisor can help you determine the best way to prepare yourself for your specific retirement needs.

Mistake #3: Not Saving Consistently

One of the worst retirement mistakes to avoid is saving too little now and hoping you can ‘catch up’ in the future. The truth is, catching up rarely happens, and unexpected life circumstances can make catching up impossible in some cases.

According to the Center for Retirement Research at Boston College, the median retirement account balance for 55 to 64-year-olds was just over $110,000. If this money had to stretch over 20 to 25 years (which it likely will as people are living longer), it amounts to just over $400 per month to live on. We can see this is just not realistic in today’s world.

To save more, create a budget, cut out unnecessary spending, open a 401(k) through your employer or an individual retirement fund as a self-employed individual, and save extra money with each raise or bonus you receive from work. Working with a financial advisor is one way to shed light on other financial strategies to boost your retirement savings.

Mistake #4: Not Factoring Taxes into the Equation

Another common mistake made during retirement is forgetting about taxes and their effect on your savings. Tax deductions change for many people once in their in retirement, and some retirees end up paying more in taxes. Consider speaking with a financial professional about tax-free withdrawals from Roth IRAs or about timing withdrawals from accounts that will be taxed.

Want to avoid other retirement saving mistakes and create a personalized retirement plan? Contact us today for a complimentary consultation.

Sources

https://www.fool.com/retirement/general/2016/01/26/20-retirement-stats-that-will-blow-you-away.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Paragon Wealth Strategies, LLC [“Paragon”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Paragon. Please remember that if you are a Paragon client, it remains your responsibility to advise Paragon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Paragon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Paragon’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.wealthguards.com. Please Note: Paragon does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Paragon’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Also Note: IF you are a Paragon client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.